This article is for informational and educational purposes only. It does not constitute financial advice. Always consult a qualified financial advisor before making any investment decisions.

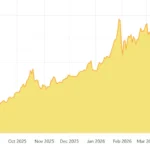

Platinum hit $2,920 per troy ounce in January 2026 — its highest level in nearly two decades. For anyone asking why is platinum so expensive, the short answer is: geology, geopolitics, and an industrial dependency that no other metal can replace. The full answer is far more interesting.

Most people assume platinum costs what it does simply because it’s rare. Rarity plays a role, absolutely. But the deeper forces driving the price in 2026 are structural — four consecutive years of supply deficits, a mining industry that physically can’t grow fast enough, and a global clean energy transition that is quietly creating an entirely new category of demand that the market isn’t fully pricing in yet.

The Ground Itself Makes Platinum Expensive

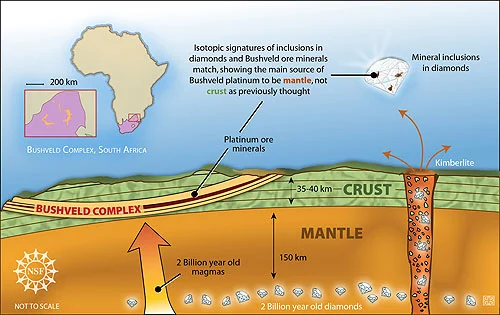

Start with the geology. According to the U.S. Geological Survey, the average concentration of platinum in the Earth’s crust is estimated at roughly 0.005 parts per million. That means for every million kilograms of crustal material, only five grams are platinum. Even within that, platinum deposits are extraordinarily localized — more than 70% of global platinum production comes from a single geological formation: the Bushveld Igneous Complex in South Africa.

Source: National Science Foundation, Public domain, via Wikimedia Commons

Compare that to gold, which is scattered across multiple continents in economically viable forms. Platinum has nowhere near that geographic spread. When something goes wrong in South Africa — a power outage, flooding, a labour dispute — the global supply of platinum tightens immediately. There is no backup source capable of filling the gap.

Refining platinum ore is a costly and laborious process. It can take from eight weeks to six months to process a batch of ore, and it can take up to 12 tons of ore to produce a single troy ounce of platinum. Gold, by comparison, requires roughly 2–3 tons of ore per ounce. That gap in extraction intensity is a direct cost that gets priced into every troy ounce sold on the market.

Source: Smithsonian Institution, CC0, via Wikimedia Commons

The platinum mining process typically takes five to seven months and it costs about $1,800 to produce one ounce of platinum. When spot prices dip below that production cost — which happened repeatedly between 2015 and 2020 — mines don’t become profitable overnight just because demand ticks up. It takes years to build new capacity. That lag is permanently embedded in the price structure.

Anyone studying why is platinum so expensive quickly realizes the answer starts kilometers underground, long before the metal reaches any exchange.

Four Years of Deficit — and Inventories Running Thin

Supply constraints alone don’t tell the whole story. Demand has compounded the pressure severely.

New projections from the World Platinum Investment Council (WPIC) show a deficit of about 240,000 ounces for 2026 following a significantly larger shortfall of 1.082 million ounces in 2025. That makes 2026 the fourth consecutive year the global platinum market has consumed more than it produced. Above-ground stocks — the buffer that keeps prices stable during short-term supply shocks — have been drawn down steadily across all four years.

Four consecutive deficit years have reduced above-ground inventories to approximately four months of demand coverage, the threshold below which spot prices respond disproportionately to operational disruption rather than to demand variability. Four months. That’s not a safety cushion — it’s a warning level.

South African primary platinum output declined from approximately 5.3 million ounces in 2006 to approximately 3.9 million ounces in 2025, a reduction of roughly 26% sustained across multiple commodity price cycles, including periods when platinum traded above $2,000 per ounce.

Standard economics says higher prices attract new investment and new supply. Platinum has repeatedly broken that rule. Industry leaders warn of an “irreversible terminal decline” due to aging infrastructure and rising costs, with major producers like Impala Platinum scaling back operations and resulting in significant job losses and a stagnant supply base that cannot keep up with demand.

This is the counter-intuitive reality that answers why is platinum so expensive even when prices are already elevated: the price signal isn’t generating new supply, because the structural barriers to building new mines are simply too high.

What Experts Say: Industrial Demand No Other Metal Can Replace

Gold’s price is driven largely by investor sentiment, central bank buying, and inflation hedging. Platinum is different. A significant share of its demand is non-discretionary — industries that require platinum specifically because no substitute works.

Automotive applications account for over 44% of global platinum demand, making it the largest use category. Catalytic converters need platinum to reduce vehicle emissions. Every petrol and diesel vehicle on the road uses platinum in its exhaust system. Tightening emission standards globally — Euro 7 in Europe, China VI-b in China — are actually increasing the amount of platinum required per vehicle, not decreasing it.

Then there’s the hydrogen economy. No commercially validated platinum replacement for PEM fuel cells exists as of mid-2026, and most industry projections maintain platinum as the primary catalyst material through at least the mid-2030s. Proton exchange membrane (PEM) fuel cells — the technology powering hydrogen trucks, buses, and industrial equipment — require platinum catalysts to function. By the end of 2025, China had established the world’s largest hydrogen vehicle ecosystem, with nearly 40,000 fuel cell electric vehicles on its roads and 574 hydrogen refuelling stations in operation.

Projections show that platinum demand from electrolyzers and fuel cells will reach nearly 900,000 ounces by 2030. That number is being added on top of existing automotive and industrial demand — not replacing it. Investors who understand why is platinum so expensive at a fundamental level recognize that this dual demand structure, combustion engines today and hydrogen tomorrow, creates a floor that pure investment metals like gold don’t have.

What People Get Wrong About Platinum’s Price

The most common misconception is that platinum should always cost more than gold. For most of the 20th century it did. At the beginning of 2000, platinum was trading at around $450 per ounce, and it reached a peak of about $2,270 per ounce in May 2008, driven by a weakening U.S. dollar and a drop in supply from South African mines. Then the financial crisis hit, and platinum fell faster than gold because industrial demand collapsed.

Gold is currently trading near twice the price of platinum, despite platinum being rarer. That gap confuses new investors. They see it as proof that platinum is undervalued. The reality is more nuanced — platinum’s price is far more sensitive to economic cycles than gold’s because of its industrial demand dependency. When manufacturing slows, platinum demand drops in ways that pure monetary metals don’t experience.

Here’s what that means practically: if you’re evaluating why is platinum so expensive purely through the lens of rarity versus gold, you’re missing half the picture. The industrial demand factor cuts both ways — it creates powerful price floors during economic expansions, and it creates meaningful price risk during recessions.

Fears over new import duties have already prompted investors to shift platinum stocks into US warehouses, tightening supply in London and triggering squeezes that helped propel prices higher in 2025 and into 2026. Trade policy, not just geology, is now a live price driver.

Why Is Platinum So Expensive in 2026 Specifically?

As of early 2026, several forces converged simultaneously. Platinum prices averaged US$2,206 per ounce in the first quarter of 2026, up 30% from the previous quarter, according to the World Bank’s April Commodities Price report.

The widening supply gap was largely driven by strong investor interest, with demand surging 65% year over year, while jewellery demand rose 9%, its strongest performance since 2018. Meanwhile, total platinum mine supply in 2025 fell 5% year-over-year to 5.51 million ounces per WPIC, running 10% below the pre-COVID five-year average.

China’s growing demand for platinum and silver markets was a major driver of the 2025 rally and is likely to remain significant into 2026. China launched new platinum and palladium futures contracts on the Guangzhou Futures Exchange in late 2025, which immediately boosted local trading activity and helped drive prices higher.

Bank of America Global Research raised its 2026 platinum price forecast to $2,450 per ounce from $1,825 per ounce in January 2026, citing persistent market deficits and trade-related supply dislocations keeping the market structurally tight.

Past performance does not guarantee future results.

The Recycling Factor — A Partial Fix, Not a Solution

One point often overlooked when discussing why is platinum so expensive: recycling now supplies a meaningful share of the market, but it isn’t enough.

Total supply is expected to reach 7.37 million ounces in 2026, up 2% year-on-year, driven mainly by higher recycling volumes. Recycling supply is forecast to rise 9% as elevated prices encourage the recovery of platinum from used catalytic converters and jewellery resale.

That’s good news. But recycling growth is largely reactive — it accelerates when prices are already high. It doesn’t prevent deficits from forming in the first place. Current recycling rates for fuel cell catalysts remain below 30%, constrained by collection logistics and technical hurdles in platinum recovery. As hydrogen fuel cell adoption grows, a new stream of platinum will eventually become recoverable — but the infrastructure to capture it doesn’t yet exist at scale.

Recycling smooths the edges of the supply problem. It doesn’t solve it.

What This Means for Investors

Understanding why is platinum so expensive matters beyond simple curiosity — it directly shapes how the metal behaves in a portfolio.

- Platinum’s price is more volatile than gold’s because industrial demand rises and falls with economic cycles

- Supply cannot respond quickly to price signals — new mine development takes years, not months

- The hydrogen economy represents genuine new demand that wasn’t a factor a decade ago

- Four consecutive deficit years have left inventories at critically low levels heading into the mid-2020s

- Trade policy — particularly US tariff risks and China’s Guangzhou futures market — is now a live price variable

The key drivers of platinum’s price rally in 2025 — strong supply/demand fundamentals, a depletion of above-ground stocks, and macropolitical uncertainty-driven precious metals demand — are expected to persist in 2026, according to WPIC Research Director Edward Sterck.

For investors tracking precious metals in 2026, why is platinum so expensive isn’t just an academic question. It’s the foundation of any serious analysis of where the metal is headed next.

Also Read: 400 oz Gold Bars: The Real Story Behind the World’s Biggest Brick

FAQ

Why is platinum so expensive compared to gold right now?

Platinum is genuinely rarer than gold geologically, but gold currently trades at nearly twice platinum’s price. The gap exists because platinum’s price is heavily tied to industrial demand, which fell sharply after the 2008 financial crisis and again during the diesel emissions scandals of the mid-2010s. Gold benefits from consistent central bank and investor demand regardless of economic cycles.

Does platinum’s price go up during recessions?

Unlike gold, platinum typically falls during economic downturns because over 44% of its demand comes from automotive manufacturing, which slows sharply in recessions. This industrial dependency makes platinum more price-volatile than gold across economic cycles.

Is platinum harder to mine than gold?

Producing one troy ounce of platinum requires processing up to 12 tons of ore and takes five to seven months from extraction to refined metal. Gold requires roughly 2–3 tons of ore per ounce. The additional energy, labour, and processing time are all embedded directly in platinum’s market price.

Will hydrogen fuel cells increase platinum demand significantly?

Platinum-based catalysts dominate the hydrogen fuel cell market with approximately 70% usage share as of 2026, according to market data. Demand from electrolyzers and fuel cells is projected to reach nearly 900,000 ounces annually by 2030 — a major new demand stream on top of existing automotive use.

Is the platinum market currently in deficit?

The WPIC projects a 240,000-ounce deficit for 2026, marking the fourth consecutive year of undersupply. The 2025 deficit reached 1.082 million ounces — the deepest shortfall recorded in WPIC data going back to 2014.

This article is for informational and educational purposes only. It does not constitute financial advice. Always consult a qualified financial advisor before making any investment decisions. Past performance does not guarantee future results.