This article is for informational and educational purposes only. It does not constitute financial advice. Always consult a qualified financial advisor before making any investment decisions.

Here’s something most gold price forecast 2050 articles won’t tell you: no financial institution publishes a verified 25-year gold price target. Not Goldman Sachs. Not J.P. Morgan. Not the World Gold Council. What exists instead is a framework — a set of structural forces that allow analysts to model scenario ranges, and those ranges tell a genuinely compelling story about where gold could sit by mid-century.

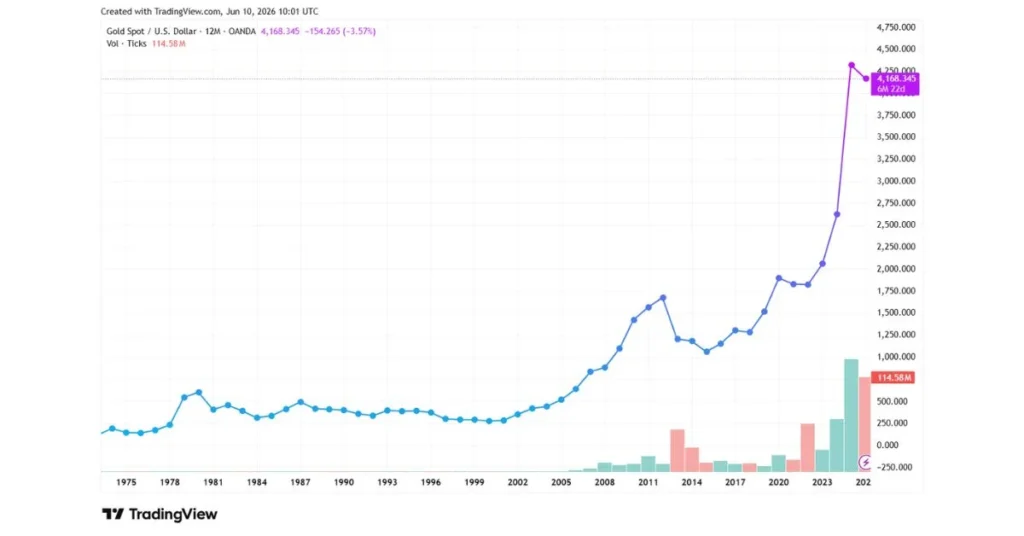

The gold price forecast 2050 discussion matters right now because gold has already done things in 2025 and 2026 that analysts thought were 2030 problems. The metal hit $5,589.38 per troy ounce on January 28, 2026 — a level that represented the most aggressive bullish forecast just 18 months earlier. Understanding what comes next requires going beyond price targets and into the structural forces that will shape the gold market over the next 25 years.

Why Any Gold Price Forecast 2050 Starts With Supply, Not Demand

Most investors focus on the demand side when thinking about long-term gold prices. That’s the wrong starting point. The more powerful variable — and the one hardest to reverse — is supply.

Global mine production has essentially plateaued over the past 5–7 years. Many of the richest historical gold regions are now in decline. South Africa’s Witwatersrand Basin, which alone yielded an estimated 30–40% of all gold ever mined, saw annual output fall from a 1,000-tonne peak in 1970 to just 157 tonnes in 2017. That’s an 84% collapse from a single region that once defined global supply.

The pipeline problem compounds this. Developing a new gold mine takes an average of 20.8 years globally due to permitting, environmental reviews, and engineering hurdles — meaning even a major discovery made today wouldn’t produce gold until the 2040s. And major discoveries aren’t happening at the rate needed. According to S&P Global analyst Paul Manalo, there have been only five major gold discoveries since 2020, totaling 17 million ounces. Matthew Miller of CFRA Research noted that “gold miners are struggling to grow reserves in line with their production.”

The World Gold Council’s analysis, produced in conjunction with Metals Focus, projects that global mined gold production is likely to gradually plateau over the next few years rather than peak sharply — though declining reserves, operational disruptions, and rising capital expenditure costs may limit any upside in production volumes.

The practical consequence for long-term gold investors: if production flatlines or contracts through 2040 and 2050, the supply side becomes structurally bullish without any demand catalyst required to push prices higher. That’s a very different dynamic from most commodities.

The US Geological Survey identifies roughly 54,000 metric tonnes of identified global gold reserves. If no significant new reserves are found, Earth’s economically extractable gold could be largely depleted by 2050. One notable 2024 discovery — a massive deposit in China estimated at over 1,100 metric tonnes — sits approximately 3 kilometres underground, near the operational limits of current mining technology.

The Scenario Framework: Three Gold Price Forecast 2050 Ranges

Because 25-year projections carry enormous uncertainty, serious analysts present gold price forecast 2050 discussions in terms of scenarios rather than point estimates. The three most consistently cited frameworks are:

Conservative scenario: Global growth stabilizes, inflation is controlled, and central bank gold accumulation normalizes. Under this conservative model, gold prices through 2050 are projected in the $2,500–$3,500 range. This scenario assumes that the geopolitical and inflationary pressures of the 2020s prove temporary, and that gold returns to being a niche portfolio asset rather than a primary safe-haven trade.

Base scenario: Real interest rates stay persistently low, central bank and ETF holdings remain elevated, and gold consolidates structural gains from the 2020–2026 rally. Under this model, gold would trade considerably higher than today’s levels through mid-century, with prices reflecting both monetary inflation and ongoing reserve diversification demand.

Bullish scenario: The bullish gold price forecast for 2050 suggests a range of $20,000–$25,000 per ounce, influenced by long-term inflation trends, central bank policies, global demand growth, and supply constraints. This scenario assumes compounding structural demand, a weakening dollar cycle, and the peak-gold supply cliff materializing as projected.

And then there’s the extreme bull case. Some analysts argue that gold could exceed $50,000 per ounce by 2050, with high demand from central banks and retail investors cited as the primary growth driver. The main stimulating factors are inflation and the increase in money supply.

That $50,000 figure isn’t widely accepted — but it’s not entirely without logic either. At a compounded annual growth rate of roughly 7% from today’s $4,500 levels, gold would reach approximately $37,000 by 2050. The question is whether the structural forces in place are strong enough to sustain that pace.

What Central Banks Are Actually Doing — and Why It Defines the Gold Price Forecast 2050

The gold price forecast 2050 conversation cannot be separated from central bank behaviour. This is the demand driver that most retail investors underestimate — and the one that most fundamentally changed after 2022.

Goldman Sachs estimates central bank demand is running at approximately 60 tonnes per month as of 2026 — a rate sustained by a structural shift in reserve management policy, not temporary buying. Central banks have now been net buyers of gold for three consecutive years above 1,000 tonnes annually.

Bank of America has argued that central banks currently hold about 10% of their reserves in gold — and that this percentage could rise to more than 30%, which would provide massive structural support for gold prices over the long term. The shift away from US dollar-denominated assets is partly policy-driven and partly structural, following the precedent of Russian dollar-reserve freezes in 2022 that prompted emerging-market central banks to reconsider their reserve composition.

Central bank diversification away from USD assets is accelerating across emerging markets, and persistent fiscal deficits in major economies are increasing long-term inflation risk. Both of those trends — if sustained — point toward structurally higher gold demand for decades.

Which brings us to the counter-intuitive insight most gold price forecast 2050 analyses miss: central bank demand is inelastic to price. Individual investors sell when prices fall. Central banks don’t. They buy on weakness, buy on strength, and treat gold as a strategic reserve asset with a 100-year time horizon. That behaviour creates a demand floor that didn’t exist to the same degree 30 years ago.

What the Research Shows: The Inflation-Gold Link Through 2050

Gold’s relationship with inflation is well-documented but frequently misunderstood. The popular version — “gold goes up when inflation goes up” — is too simple. What actually drives gold is the real interest rate: the nominal rate minus inflation. When real rates are negative or near-zero, gold’s opportunity cost collapses and its appeal surges.

The long-term gold price forecast to 2050 embeds expectations of periodic inflationary waves. Gold remains one of the few assets consistently immune to currency debasement.

The important structural point: every major economy running persistent fiscal deficits is effectively committed to either inflation or financial repression as its exit strategy. The US national debt trajectory, Japan’s debt-to-GDP ratio, and the EU’s fiscal pressures all point toward long-term environments where real interest rates stay structurally low. The convergence of multiple structural factors — supply constraints, central bank demand, geopolitical uncertainty, and inflation concerns — suggests a constructive long-term outlook for gold prices through 2050.

Investors who track gold closely know that the metal doesn’t need all of these factors simultaneously. Any two or three, sustained over a decade, are typically enough to produce a meaningful multi-year bull market.

Near-Term Waypoints: 2030 and 2040 in the Gold Price Forecast 2050 Picture

Since no analyst publishes a direct 2050 target, understanding the gold price forecast 2050 means working through the intermediate milestones where analyst consensus is more developed.

For 2030: Most analyst consensus suggests gold will appreciate from current levels to $5,000–$5,400 by 2030, with moderate forecasts representing the central case. More aggressive forecasters see higher targets: J.P. Morgan projects $6,300 citing a structural demand thesis from central bank accumulation. Deutsche Bank and Yardeni Research align near $6,000. Goldman Sachs maintains a $5,400 target based on continued de-dollarisation.

For 2027, already within near-term visibility, InvestingHaven projects gold approaching $6,500, citing a secular bull market confirmed by 50-year chart patterns.

By 2035, scenario-based projections from CoinPriceForecast model a steady upward trajectory with year-end prices rising from $8,930 in 2030 to $10,091 in 2031, $11,194 in 2032, and continuing higher through 2035. These aren’t consensus banker targets — they’re model outputs — but they illustrate the compounding trajectory that supply constraints and monetary debasement imply.

By 2040: Long-term reserve depletion modelling suggests significant production capacity loss by 2040–2050, unless substantial new discoveries replace depleting reserves. That supply cliff, if it materialises as current trajectory suggests, coincides with peak global demand from Asian middle-class growth.

What People Get Wrong About the Gold Price Forecast 2050

The most common mistake is treating any single number — $10,000, $20,000, $50,000 — as a prediction rather than a scenario output. Long-term price forecasting is fundamentally probabilistic. Anyone claiming to know gold’s price in 2050 with precision is confusing a model assumption with a fact.

The second error: assuming gold’s historical correlation with inflation will hold in its simple form. Gold underperformed inflation for significant stretches of the 1980s and 1990s when real interest rates were high. The gold price forecast 2050 hinges not on inflation alone but on real rates, dollar strength, geopolitical architecture, and reserve policy — none of which are predictable over 25 years.

Third mistake: ignoring the technology wildcard. Asteroid mining, deep-sea extraction, and advances in low-grade ore processing could theoretically expand supply in ways current reserve data doesn’t reflect. In 2024, geologists discovered a massive new gold deposit in China estimated to contain over 1,100 metric tonnes — but it sits approximately 3 kilometres underground, near the limits of current extraction technology. The supply constraint thesis holds unless extraction technology makes a generational leap.

Gold Price Forecast 2050: The Honest Investor’s Summary

As of 2026, the structural case for gold over the next 25 years is stronger than it has been at any point in modern financial history. Supply constraints from annual production growth limited to 1–2%, de-dollarisation, geopolitical fragmentation, and central bank reserve accumulation are all compounding in the same direction.

The gold price forecast 2050 most defensible by data sits in a wide range: conservative models suggest $3,500–$5,000 in today’s purchasing power terms; base scenarios imply $10,000–$15,000 in nominal terms; and the bullish scenarios, which align with a “peak gold” supply crisis and continued monetary debasement, suggest $20,000–$25,000 or beyond.

What the data doesn’t support is a dramatic collapse. The structural demand floor from central banks, the supply plateau, and the monetary system’s dependence on inflation as a fiscal tool all point the same direction — up. How far up remains, genuinely, the most uncertain question in commodity markets.

Past performance does not guarantee future results.

Also Read: How Much Is 100 Dollars of Gold? The Surprising Real Answer

FAQ

1. What is the gold price forecast for 2050?

No single verified consensus exists, but scenario models range from $3,500 (conservative) to $20,000–$25,000 (bullish) per troy ounce, with the wide spread reflecting genuine uncertainty about monetary policy, supply depletion, and geopolitical structure over a 25-year horizon.

2. Will gold reach $10,000 per ounce before 2050?

Multiple analysts and scenario models project gold reaching five-digit prices before 2050 under base and bullish scenarios. Libertex’s scenario modelling shows year-end prices above $10,000 by 2031 in its upside scenario, driven by peak-gold supply constraints and central bank demand.

3. What is the biggest driver of gold prices over the long term?

Central bank reserve policy is the most powerful structural driver, because central banks are inelastic buyers — they accumulate gold regardless of short-term price. The World Gold Council confirmed central banks added 244 tonnes to global reserves in Q1 2026 alone, continuing a streak of 1,000+ tonne annual purchases.

4. Is the “peak gold” theory real?

The USGS identifies approximately 54,000 metric tonnes of identified global gold reserves. At current extraction rates, economically viable gold could be largely depleted by 2050 absent major new discoveries — a supply scenario that hasn’t happened with this degree of urgency in modern market history.

5. How should investors use a gold price forecast 2050 in their portfolio strategy?

As a directional framework, not a trading target. Long-term gold price forecasts identify structural forces — supply constraints, monetary debasement, central bank demand — that justify holding gold as a portfolio hedge over multi-decade timeframes. Specific allocation decisions should always be made with a qualified financial advisor.

This article is for informational and educational purposes only. It does not constitute financial advice. Always consult a qualified financial advisor before making any investment decisions.