This article is for informational and educational purposes only. It does not constitute financial advice. Always consult a qualified financial advisor before making any investment decisions.

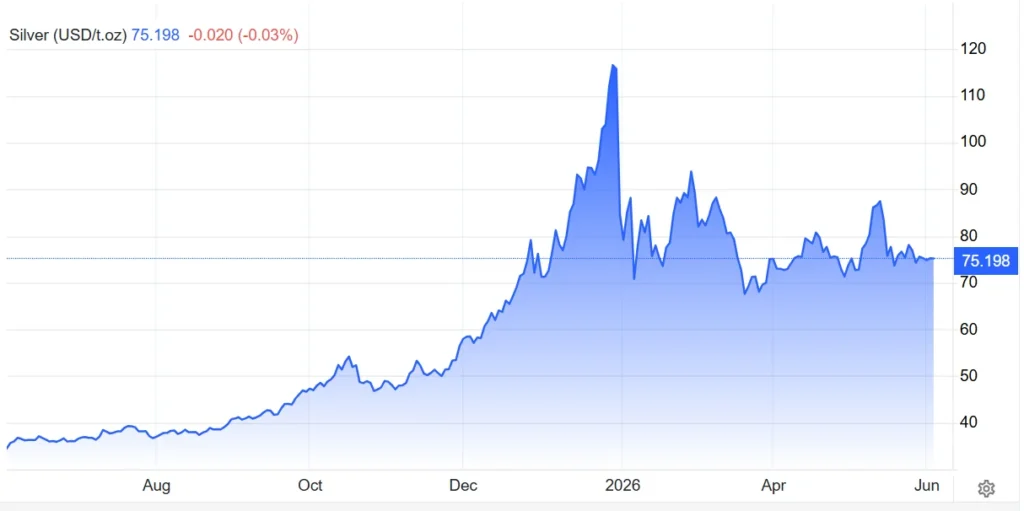

Picture a commodity consumed faster than it’s mined — every single year — for six consecutive years. No dramatic headlines. No government emergency. Just a quiet, relentless drawdown of global reserves that the mainstream financial press mostly ignored until silver hit $116.58 per troy ounce in January 2026. That’s the silver shortage in a sentence. And by the time most investors noticed it, the bulk of the structural damage was already done.

Six Years Running: What the Silver Shortage Actually Looks Like

According to the Silver Institute’s latest World Silver Survey, produced alongside London-based consultancy Metals Focus, the global silver market will record a 46.3 million ounce shortfall in 2026, widening from a 40.3 million ounce deficit in 2025 — a 15% increase in the annual shortfall.

That number sits inside a much larger story. Consecutive silver supply deficits have collectively absorbed an estimated 762 million ounces from global above-ground stocks since 2021. To understand the scale: that cumulative 5-year deficit has climbed above 800 million ounces — equivalent to an entire year of global mine output, gone.

A structural deficit is not a temporary shortage caused by a factory fire or a shipping delay. It is a condition in which the global market consistently produces less of a commodity than it consumes, year after year, drawing down existing reserves to bridge the gap.

The practical consequence for investors is direct: when above-ground stocks fall, the buffer that stabilises prices shrinks. Sudden demand spikes — from any direction — have less cushion to absorb them. The October 2025 liquidity squeeze in the benchmark London market was a direct result of that process, triggered by months of inflows into US inventories and silver-backed exchange-traded products alongside a spike in physical demand — driving prices to their record high of $116.58 per ounce in January 2026, following a 147% surge in 2025.

Why Silver Supply Can’t Simply Be Turned Up

Here’s where most commentary on the silver shortage falls short. Readers assume that higher prices fix supply problems — miners dig more, problem solved. Silver doesn’t work that way.

Approximately 70% of all silver mined globally is extracted as a byproduct of other mining operations, primarily lead, zinc, and copper. Silver output is fundamentally governed by the economics of entirely different metals. When copper prices fall and copper mines scale back, silver output drops regardless of where silver spot prices are trading. That structural dependency breaks the normal feedback loop between price and supply response.

Global silver mine production is projected to exceed 27,000 metric tonnes in 2025, with only a modest increase in 2026 — and output stability depends entirely on sustained throughput at major sites in Mexico, Peru, and China, as well as strong output from base-metal operations underpinning byproduct supply.

New silver mines take 10 to 15 years from discovery to production. No mine opened in 2026 was conceptualised in response to the current deficit. The supply pipeline that exists today reflects investment decisions made when silver was trading at $15–$20 per ounce. Anyone who has studied silver markets understands this lag is the single most underappreciated factor in the shortage equation.

What Experts Say About the Silver Shortage in 2026

Not every analyst agrees on the scale of the problem — which itself tells you something important.

UBS strategists Wayne Gordon and Dominic Schnider project the 2026 silver supply deficit to narrow to roughly 60–70 million ounces — a dramatic reduction from a prior estimate of 300 million ounces, citing weaker investment demand, softer industrial consumption from photovoltaics due to elevated prices, and higher mine supply. Their base case: silver trades broadly sideways.

The Silver Institute sees the picture differently. Their data shows the deficit widening, driven by a retail investor surge replacing the industrial demand that high prices have begun to erode. Global coin and net bar demand rose 14% in 2025, supported by a 33% jump in physical investment in India, while ETPs recorded net inflows of 68.3 million ounces. The Institute forecasts an 18% increase in physical investment in 2026, reaching the highest level since 2022, driven largely by a 57% US retail demand rebound.

Frank Holmes, CEO of US Global Investors, reports that RBC expects the physical silver market to remain tight in the near term, projecting a gold/silver ratio of 60–65 over the next few years. Covered silver producers and precious metal royalty equities are currently pricing an average silver price of $122 per ounce — well above recent spot levels.

The divergence between UBS and the Silver Institute isn’t noise. It reflects a genuine split in the market between paper silver dynamics and physical silver realities.

The Industrial Machine That Keeps Consuming Silver

Gold sits in vaults. Silver gets used up.

Silver’s industrial consumption hit 680.5 million ounces in 2024 — a record high for the fourth consecutive year, accounting for 59% of total silver demand, up from roughly 40% just two decades ago.

Industrial use accounted for around 60% of total global silver demand in 2024. Looking ahead, global solar PV capacity is forecast to reach 665 GW in 2026, supporting around 120–125 million ounces of silver demand from solar panels alone. Electric vehicle production, forecast at 14–15 million units, is expected to add a further 70–75 million ounces, while grid upgrades and data centre infrastructure could contribute an additional 15–20 million ounces.

Each battery-electric vehicle consumes on average 67–79% more silver than an internal combustion engine vehicle, with approximately 25–50 grams of silver per EV. And the Silver Institute’s December 2025 report confirms that sectors including solar energy, automotive EVs, and data centres and AI will drive industrial demand higher through 2030.

Which brings us to a counter-intuitive insight most investors miss entirely: manufacturers don’t stop needing silver because the price goes up. The EU’s renewable energy mandates don’t pause for commodity prices. A solar cell without silver paste doesn’t conduct electricity. This isn’t investment demand that disappears when sentiment shifts, or jewellery demand that fades when prices rise. It’s industrial consumption driven by government mandates and technological necessity.

What People Get Wrong About the Silver Shortage

The most common misconception: that “paper silver” and physical silver are the same thing.

They aren’t. Exchange-traded silver — futures contracts on COMEX, ETPs, and other instruments — represents claims on silver that may or may not be fully backed by physical metal. While exchange-traded paper silver exists in abundance, physical silver is increasingly scarce, with major inventories in London, New York, and Shanghai experiencing rapid depletion.

The second error is assuming recycling will close the gap. Recycling contributes meaningfully to silver supply, but it can’t scale fast enough to offset a 46-million-ounce annual structural deficit. Most recycled silver comes from photographic and industrial waste streams — categories that have either already declined (photography) or are consuming silver faster than they’re returning it (solar panels now being installed, not yet reaching end-of-life).

And the third — and most damaging — misconception is that the silver shortage only matters to silver investors. Sustained high prices are forcing solar panel manufacturers and jewellery fabricators to actively cut silver from their supply chains. If silver becomes structurally scarce at scale, clean energy infrastructure timelines get disrupted. The shortage isn’t contained to a commodities spreadsheet.

How the Silver Shortage Affects Premiums and Availability

When the deficit tightens exchange-held inventory, the first thing retail buyers notice is dealer premiums rising above spot price. A standard 1-ounce silver coin that might have traded at $2–$3 above spot in a balanced market can jump to $6–$10 above spot during a physical squeeze.

The silver market has been trading on a structure that has been in deficit for six consecutive years, and the October 2025 London liquidity squeeze was caused not by a geopolitical shock or supply disruption but by the ordinary mechanics of accumulated drawdown — inflows into US inventories and exchange-traded products triggered a chain reaction in a market with insufficient physical buffer.

For buyers of physical silver — coins, bars, and rounds — the silver shortage changes the calculus of timing. Waiting for the “right price” on spot may mean paying a significantly higher premium if dealer inventory tightens during a demand spike. As of 2026, that risk is no longer theoretical. It already happened once.

Also Read: How to Invest in Gold for Beginners: The Real 2026 Guide

FAQ

Is there actually a physical silver shortage right now?

There is a significant, ongoing structural shortage of physical silver in 2026, marking six consecutive years of deficits where industrial and investment demand outweighs supply, with major inventories in London, New York, and Shanghai experiencing rapid depletion.

How much silver has been drawn from global reserves during the current shortage?

Cumulative deficits since 2021 have drawn more than 800 million ounces from above-ground stocks, roughly equivalent to an entire year of global mine production.

Why can’t miners produce more silver to end the shortage?

Because approximately 70% of all silver mined globally is produced as a byproduct of copper, lead, and zinc mining. Silver output is governed by the economics of base metals, not silver prices, meaning new silver supply cannot respond quickly to rising prices.

Does the silver shortage affect solar panel and EV manufacturing?

Sustained high prices are already forcing solar panel manufacturers and jewellery fabricators to cut silver from their supply chains, though EV and grid infrastructure demand continues to grow regardless of price pressure.

Will the silver shortage push prices higher in 2026?

Analysts disagree. UBS projects silver to trade broadly sideways in their base case, forecasting the deficit will narrow to 60–70 million ounces. RBC and US Global Investors’ Frank Holmes take a more bullish view, with silver royalty equities currently pricing an average of $122 per ounce. Past performance does not guarantee future results.

This article is for informational and educational purposes only. It does not constitute financial advice. Always consult a qualified financial advisor before making any investment decisions.